In June 2026, Honza and I held the very first meeting of Opatov Finance Society – and the club's official founding meeting. We met up at our gymnázium, put up a presentation called "Time Is Your Capital", and talked through why we're actually starting this club and what we want it to become.

Why Starting Early Matters

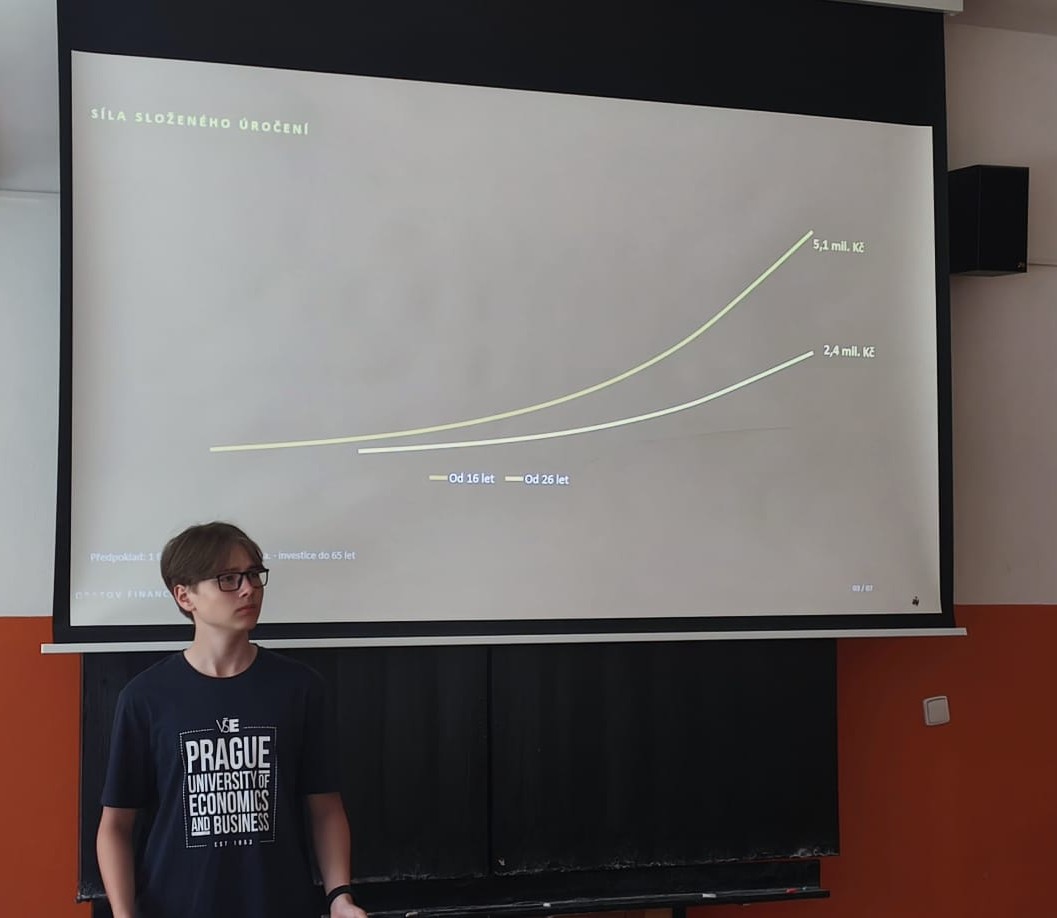

The core idea behind the whole intro was simple: someone who starts investing at 16 has a ten-year head start on someone who starts at 26. Ten extra years sounds like a small detail at first, but the numbers tell a very different story.

Compound Interest in Practice

We walked through a concrete example: investing 1,000 CZK a month at an average 7% annual return, until age 65, starting at 16 grows to roughly 5.1 million CZK, while starting at 26 grows to about 2.4 million CZK. Same monthly amount, different starting point, more than double the outcome. That's the power of compound interest that everyone talks about but rarely sees laid out this clearly.

The Three Pillars of the Program

We spent the rest of the meeting on how the club will actually run. The program rests on three pillars:

- Market Analysis: regular discussions of what's currently happening in the markets.

- Education: workshops and simulations instead of classic lectures, so we actually get to try investing hands-on.

- Guests From the Industry: inviting people who invest for a living to share real experience with us.

What's Next

We also confirmed the club's format at the meeting – we'll be meeting once a month. Now we're moving into member recruitment, running from May through September 2026, with a goal of 15+ active members before our first industry guest joins us in the fall.

If finance, investing or economics interests you and you'd like to join, check out our registration form – we meet once a month and new members are always welcome.